FAQs About 529 Plans

This week we are focusing on a practical question for parents when it comes to college and career planning for their children. We are talking about saving money for college through a 529 plan.

Here are a few questions that many people have about 529 plans:

- Should I open a 529 for my kids?

- What if my kids don’t go to college?

- What are the advantages and disadvantages?

- What if I don’t have a lot of money to put in? Is it still worth it?

And to help us answer these questions, I’m excited to introduce someone who has been a tremendous financial advisor to me for a number of years. We talked at length about 529 plans, and I’m sharing a snippet of our conversation here:

Interview With Michael Walton

Me: Could you tell the audience a little about who you are and what you do?

Michael: My name is Michael Walton and I’ve been an advisor affiliated with New York Life since 2003. I work with individuals and businesses in a variety of different planning arenas which are dependent upon individual situations and goals. Some of these planning items would include, Life, Disability, & Long-Term Care Insurance Planning, Individual and Company Sponsored Retirement Planning, and College Planning.

Me: Do you generally recommend 529 plans to clients? Why or why not?

Michael: If their main goal is to save specifically for higher education, then a 529 plan can be a great, tax-efficient tool for those savings. PA is one of the states that allows an in-state tax benefit for any state’s 529 plan (All plans are established in a specific state, but many times have no bearing on where the child attends school)

Me: What if none of my kids attend college? (If I’m reading some of the updated laws correctly, you can now roll these funds into your kid’s retirement savings with no fees).

Michael: Yes, many changes were made over the past few years which eliminated or changed some of the restrictions. 1. Withdrawals equal to scholarships are now allowed 2. You can move money from one child to another or use it for yourself without penalty 3. If the account has been opened for at least 15 years, then transfers are allowed to a Roth IRA (subject to annual limits and $35k total)

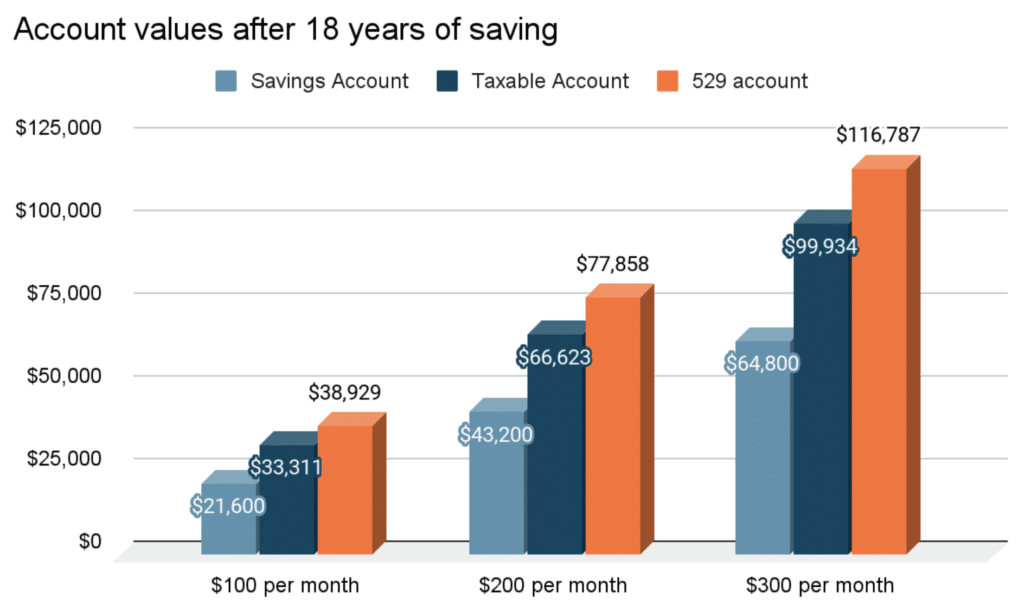

To get a better idea of the tax advantages, I asked Michael to help me calculate how a 529 plan would compare to a taxable fund account like a mutual fund in an 18 year period.

This graph assumes a 6% average annual rate of return (compounded monthly) for both investments and an effective federal income tax rate of 25% and no state income tax. The 6% APR is a conservative estimate, so there is a good chance that investors could receive even more free money in that same amount of time.

Our Personal Strategy

Now, can I be real with you? We do have 529 plans for each of our kids, but we are personally not putting a lot of money into each. There are a few reasons for that, but one big one is that we just don’t have a lot of extra money! However, I’m a big fan of compound interest (not that compound interest was looking for fans), and I’m also a big fan of not giving the government more money than I need to. Notice how putting in money into a 529 plan can nearly double your money in 18 years when compared to a savings account.

529 plans are not for everyone. When opening up a 529, you are locking in that money for a specific purpose. So even though recent laws have given more flexibility to how to spend that money (K-12 educational expenses, kids retirement, apprenticeship programs) it is important to know your goals and how you want to support your kids. So contact someone like Michael who can walk you through the decision process.

If you would like to get in touch with Michael Walton to schedule a free consultation, you can get in touch at mpwalton@ft.newyorklife.com or 717-645-1699.